FI Series #5: Save Your Way to Financial Independence

The Most Important Variable in Your FI Journey: Savings Rate

If there’s one number that determines how quickly you reach financial independence, it’s not your income or your investment return—it’s your savings rate.

Your savings rate is the percentage of your gross income that you save. And increasing it can dramatically reduce the time it takes to make work optional.

In this post, we’ll show:

Why savings rate matters more than you think

How to increase it by raising income or reducing expenses

How to make those changes sustainable over time

Why Savings Rate > Investment Returns

It’s tempting to obsess over picking the right ETF or trying to beat the market. But here’s the truth:

A high savings rate will get you to FI faster than high returns.

Example:

A 25% savings rate with 5% returns = 31.9 years to FI

with 10% returns= 22.5 years to FI

A 50% savings rate with only 5% returns = 16.6 years to FI

Even doubling your investment returns won’t cut your timeline as much as doubling your savings rate.

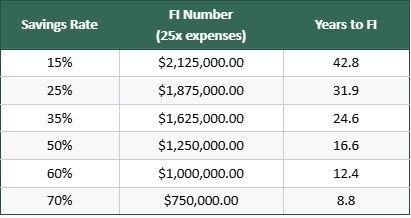

The Savings Rate Time-to-FI Table

Assuming a $100,000 income and 5% real return, here’s how long it takes to reach FI at different savings rates:

The key insight: as your savings rate increases, both your FI number and your time to reach it decrease.

Increase Savings in Two Ways: Income vs. Expenses

There are two main ways to improve your savings rate:

1. Increase Income

If you can earn more while keeping your expenses flat, your savings rate climbs fast.

Ways to grow income:

Negotiate a raise

Switch to a higher-paying job or career

Develop new skills or certifications

Start a side hustle or freelance gig

2. Reduce Expenses

Alternatively, cutting spending is often the quickest way to boost your savings rate.

Ways to reduce expenses:

Move to a lower-cost-of-living area

Downsize housing or refinance your mortgage

Drive a more affordable car (or go car-free)

Cook at home and reduce dining out

Bonus: Cutting spending reduces your FI number and increases your savings rate.

Which Is Better?

It depends. Increasing income takes time and effort but can unlock long-term gains. Cutting expenses provides immediate results and helps avoid lifestyle inflation.

Best case: Do both. Raise your income and resist the temptation to upgrade your lifestyle.

A Note on Entrepreneurship

Starting a business can be a powerful income strategy—but it comes with risk.

Reality check:

25% of small businesses fail in the first year

50% fail within five years

Entrepreneurship is often safer after reaching FI, when you’re not dependent on immediate income. But low-cost side hustles or passion projects can make sense now if approached with a lean, test-first mindset.

Final Thoughts

The fastest path to financial independence isn’t through complex investment strategies—it’s through mastering your savings rate.

Every dollar you save shortens the distance to freedom. Whether you earn $60K or $260K, what matters is how much you keep.

In the next post, we’ll talk about what to do with those savings: how to invest wisely, build a diversified portfolio, and grow your wealth over time.

Coming Next:

How to Invest for Financial Independence: Index Funds, Asset Allocation & Staying the Course

🔗 This post is part of the Financial Independence Blog Series.

Learn how to save more, invest smarter, and reach FI faster.

📖 Previous: Mindset & Habits for FI

📘 Coming Soon: How to Invest for Financial Independence